TMTB Morning Wrap

Good morning. NFP roughly inline with +227k vs expects for 200k, unemployment 411.2% vs 4.1%. Participation down, so the rise in the unemployment rate more likely driven by softer household survey gain. Overall, should provide cover for Fed to cut on 12/18.

QQQs +20bps, BTC -40bps; China +2%. 2 year dn 4bps, 10 year dn 2bps.

Lots to get to today, so let’s get straight to it…

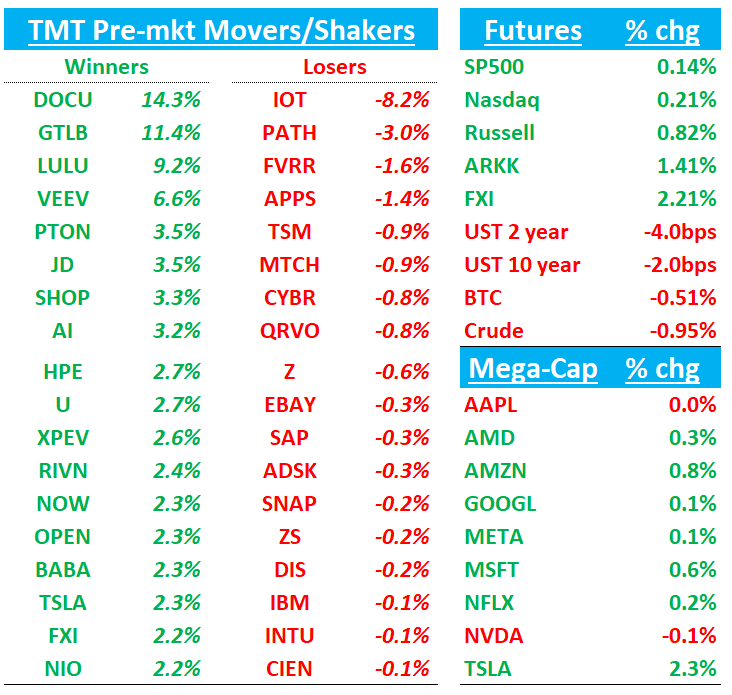

GTLB +10%: Beat and Raise with large rev beat sub acceleration, and cRPO beat

Very solid results here and not much to nitpick (net retention slightly down). Sentiment/positioning had been mixed going in so this is better than a relief for investors

Revenue grew 31% (matching last quarter), ahead of Street's 26%, with particular strength in enterprise and government sectors. Q3 beat guidance by 4%, marking strongest outperformance since Q3'24. cRPO growth at 39% versus previous quarter's 42%, while operating margin reached 13.2%, exceeding Street's 10.6% expectation. Subscription revenues slightly accelerating to grow 34%

Management raised FY25 guidance to 30% revenue growth (from 28%) and ~9% operating margin (from ~8%), with Q4 guidance modestly above consensus. Duo contribution expected to remain minimal this year before accelerating in FY26. Duo platform gaining enterprise traction with notable wins (Emirates, F5, LATAM Airlines), delivering ~25% ARR uplift and significant productivity gains. Ultimate SKU reached 48% of ARR (up from 47%), featured in 7/10 largest deals and 9/10 largest initial purchases.

New CEO Bill Staples takes over as prev CEO stepping down due to healthy reasons

Bulls will take this as validation that growth is likely to stay in ~30% range while new products coming online could materially improve tier conversions and Duo adoption over the next year.

HPE +3%: Mixed with a nice top and bottom line beat but AI rev in line at $1.5B (and below whispers of $1.7B) and orders of 500M missed street at $1.4B. Guide roughly in line. Beat driven by Hybrid cloud and EPS helped by H3C sale

Server biz continues to see momentum but its dragging gross margins down which were -390bps y/y to 39.9% lowest since Q4’20 but hybrid cloud continues to drive upside (Greenlake, storage strength) while Networking is seeing more stability. The fwd guide includes q/q stepdowns in AI server sales (Blackwell impact, Q4 AI order “de-booking” of $700M), but was still in line-ish with consensus. JNPR deal still expected to close early part of 2025.

Print shouldn’t change bulls or bears minds either way. Sentiment has turned slightly more positive here as bulls think HPE positioned for growth across multiple vectors: expected IT spending recovery driving server, storage and networking improvement; Juniper integration synergies; Hybrid Cloud momentum from private cloud AI expansion, Alletra storage, and GreenLake adoption driving ARR growth; and margin expansion potential from increasing Enterprise/Sovereign AI server demand. In addition, bulls will continue to point to valuation disparity with DELL (13x vs sub 10x P/E) and hope for share gains from SMCI’s woes.

Bears will point to continued margin pressure and lack of AI upside.

Gets and upgrade at Citi raising target to $26 from $23, citing multiple growth catalysts: improving mainstream server and enterprise networking demand, expanding AI opportunities, and potential multiple expansion versus peers. Following Q4's earnings beat, firm notes potential for increased enterprise AI and sovereign customer contributions, suggesting positive revenue and margin trajectory. Combined with strengthening core infrastructure spending and Juniper acquisition benefits, Citi likes the r/r here.

3P Roundup:

AMZN: Hearing Yip out saying NA retail now tracking 4ppts above street (was out yesterday with weekly data but hearing they put out a full note today)

W: Hearing Clev and Yip both positive on BFCM with the former now saying W tracking a couple ppts above street

META: Hearing Yip downtick in 2 weeks prior to thanksgiving (note that TikTok District court decision due today)

ETSY: Hearing 3p saying GMS continues to track 4-5ppts below street

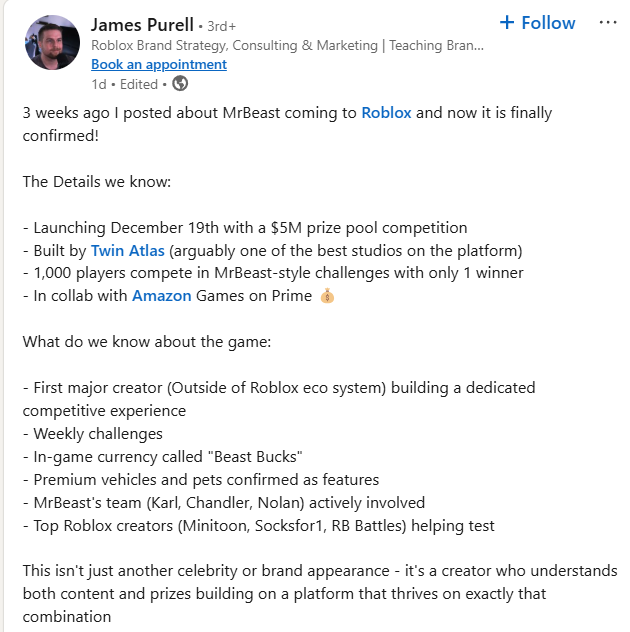

RBLX +8% strength yesterday driven by Mr.Beast hosting an event on Dec 19th

Think this is impt in terms of signaling for the platform. Mr. Beast has largest # of subs on YT with 335M

SHOP: Loop upgrades to Buy with PT of $140 up from $110

Loop upgrades Shopify to Buy from Hold, raising target to $140 from $110 (23% upside), citing underappreciated AI integration both customer-facing (Shopify Magic) and internal operations (support, sales, HR, finance).. The firm expects significant operating leverage as revenue growth outpaces operating expenses, driving margin expansion and higher valuation multiples. New target based on 16.5x 2025 revenue, aligned with large SaaS peer average.

ACN: GS Raises to buy

Goldman upgrades Accenture to Buy from Neutral, raising target to $420 from $370. Schneider cites easing cyclical pressures across IT services, particularly in financial services and healthcare verticals. As the leading global IT services provider, Accenture stands well-positioned to capture rebounding discretionary spending. The firm sees upside to consensus estimates as macro conditions improve, noting current FY25 guidance already incorporates conservative macro assumptions.

NFLX: RJ maintains Hold but notes survey improvements

RJ notes Netflix's viewer penetration shows first increase after six consecutive survey declines, reaching 56% (up from 50% in June 2024, 53% in December 2023). Growth strongest among 18-29 age group (57%, +5 points) and older demographics (57%, +13 points). RJ notes NFLX maintains dominant position in value perception, with 51% ranking Netflix in top 3 must-keep services, substantially ahead of Amazon Prime (37%) and Hulu (25%). The firm also notes Ad-supported tier gaining significant traction - 68% of Netflix users now on ad tier (up from 52%), with additional 11% expressing interest. Combined actual/potential ad tier adoption reaches 79%, marking 11-point increase over six months.

ABNB: Is New York City About to Curb Its Airbnb Crackdown?

As New York City hotel rooms reach record nightly rates, city lawmakers are proposing a bill that would walk back some restrictions on hosts of Airbnb properties and other short-term rentals.

If enacted, the bill could meaningfully boost listings, which dwindled to about 3,700 last month, compared with nearly 23,000 in January 2023, according to the market-research firm AirDNA. It also resumes the pitched battle between the hotel industry and the rental platforms, including Airbnb.

AMZN: ISI deep dives into AMZN’s Rx opportunity

ISI says their survey shows 13% of Amazon customers now purchasing pharma products, with 45% expressing strong interest in prescription purchases. The firm notes aggressive expansion of same-day prescription delivery targeting nearly 50% U.S. consumer coverage by end-2025. ISI’s industry checks suggest PillPack integration and 2025 expansion plans could be transformative. ISI’s current revenue estimated at $2B, with sensitivity analysis indicating potential for $33B incremental revenue and $1.6B operating income over 3-5 years (assuming 50% Prime household adoption, 50% Rx spend share, 5% margin), which would represent 5-10% of 2024 rev/ebit.

PTON: Peloton upgraded to Neutral from Sell at UBS

UBS raised its Peloton rating to Neutral from Sell while substantially increasing its price target to $10 from $2.50. The firm expects EBITDA to benefit from cost reductions extending beyond the announced $200M, driven largely through OpEx cuts. With expectations now reset to minimal growth over the next two years, the CEO transition presents an opportunity for further recalibration against more tempered buy-side expectations, the analyst notes. UBS views favorably the alignment of the new CEO's compensation structure with key performance metrics - revenue, operating income, EBITDA and free cash flow.

GOOGL: ISI surveys 1k people and comes away with some takeaways

ISI says their survey points to GOOGL maintaining dominant search position though showing slight decline (80% to 78%) while ChatGPT gains share (1% to 5%). However, Google's commercial search categories (Shopping & Travel) remain stable. ISI says Generative AI search tool adoption accelerating significantly, rising from 40% to 62% between June and November noting user satisfaction with Google's AI offerings (Gemini, AI Overview) shows improvement, with 71% finding them more effective than traditional search (up from 61%) and 62% reporting high satisfaction levels (up from 56%).

UBER: Jefferies reiiterates buy and $100 PT after Waymo announcement yesterday

Jefferies notes Waymo's latest initiative represents continued business model exploration rather than definitive strategy, with potential Uber partnership still viable. Uber investment thesis remains positive based on strong free cash flow growth, increasing share buybacks, reduced Didi competitive pressure, and limited impact from robotaxi developments

DOCU +14%: Strong billings beat and accel; beat and raise

Importantly, DOCU said that the core business is stabilizing, that they saw a "marginal improvement in the environment," and gone was any reference to "deal timing" issues and a tough macro.

Billings significantly outperformed at $752.3M (+8.7% Y/Y), $32M above guidance high-end and above bogeys, with early renewals driving one-third of the beat. Management highlighted improved retention and self-service growth momentum, supported by NRR returning to 100% and >10% customer growth. IAM solution showing early promise but Q3 impact limited given product maturity and deal sizes. FY26 outlook suggests continued core business stabilization and early IAM traction, though limited margin expansion expected.

Q3 metrics:

Revenue $754.8M (+7.8% Y/Y)

Subscription revenue +7.7% Y/Y

Billings accelerated to 8.7% from 1.9% last quarter

U.S. revenue growth reaccelerated to 4.7%, driven by SMB penetration

FY25 revenue guidance raised to $2,959-2,963M (7.2% growth vs previous 6.7%)

APP: Citi raises PT to $460 from $335 at Citi following mgmt meetings

Following investor meetings with AppLovin's leadership (CEO Foroughi, CFO Stumpf, IR head Hsiao), Citi expresses increased confidence in growth prospects across mobile gaming and eCommerce segments. Firm raises estimates and adjusts target multiple to better reflect peer valuations and growth trajectory.

MSFT/OpenAI: OpenAI in talks to ditch agi clause with Microsoft - FinancialTimes

FT reporting Microsoft's OpenAI investment terms may see significant revision regarding AGI access. Current agreement voids Microsoft's access rights once OpenAI achieves artificial general intelligence (defined as systems outperforming humans in most economically valuable work), with OpenAI's board determining when this milestone is reached. OpenAI's board now considering removal of this restriction, which would allow Microsoft continued investment and technology access post-AGI achievement. Change could unlock substantial future investment potential, though discussions remain ongoing with no final decision reached.

Other News:

AAPL, China: Apple reportedly plans to partner with Baidu for AI features in China during 2025, though discussions face challenges around data usage policies for model training. Sources indicate disagreement between companies regarding user data utilization approach. Commercial Times

AMD: AMD CEO Lisa Su Is Ready for the AI Spotlight– Bloomberg

Crypto: Donald Trump Names David Sacks as White House AI and Crypto Czar - Bloomberg– Bloomberg

Gen AI: xAI raised $6B in fresh capital in a deal valuing the firm at >$40B – Bloomberg

INTC: Intel’s Lack of a Clear Plan Makes Wall Street Even More Bearish - Bloomberg

SMTC: upsized underwritten 9.1M-share offering priced at $63/sh through MS & UBS